Key Takeaways

- The Registry of Moneylenders (RoM) is the official authority under Singapore’s Ministry of Law that regulates licensed moneylenders and enforces the Moneylenders Act.

- Always verify a moneylender through the official RoM list before borrowing to ensure you’re dealing with a legitimate, licensed lender.

- Licensed moneylenders must comply with strict regulations, including limits on interest rates and fees, transparent loan contracts, and proper identity verification.

- The Registry protects borrowers through oversight and enforcement, but it does not approve loan applications, negotiate loan terms, or provide loans directly.

- Avoid responding to unsolicited loan offers via SMS, WhatsApp, or social media, and report any suspicious lending activities to the relevant authorities.

Did you know that if you’re planning to borrow from a licensed money lender in Singapore, understanding the role of the Registry of Moneylenders (RoM) is one of the most important steps you can take? Operating under Singapore’s Ministry of Law, the Registry oversees the licensing and regulation of all licensed money lenders to ensure compliance with the Moneylenders Act and other relevant regulations.

Beyond regulating the industry, the Registry also helps protect borrowers from illegal lending activities.

Whether you’re considering a legal money lender, or searching for an online money lender in Singapore, verifying the lender through the Registry should always be your first step. Read on to find out more, pronto!

What Is the Registry of Moneylenders (Rom)?

The Registry of Moneylenders is the government authority responsible for regulating licensed money lenders in Singapore. As a division under the Ministry of Law, it administers and enforces the Moneylenders Act, which provides the legal framework governing the licensed moneylending industry.

This might surprise you, but its responsibilities extend beyond issuing licences. The Registry monitors compliance with legal requirements, conducts inspections, investigates regulatory breaches, and takes enforcement action when necessary. Through these measures, the Registry of Moneylenders helps maintain a transparent and well-regulated lending environment where borrowers can access loans with greater confidence.

Whether you are borrowing from a neighbourhood licensed money lender or an online money lender in Singapore that requires an in-person verification process, every legal money lender must operate in accordance with the standards set by the Registry.

What Does the Registry of Moneylenders Do?

The Registry performs several important functions to ensure Singapore’s moneylending industry remains safe, transparent, and compliant with the law.

#1 Licenses New Money Lenders

Before any business can operate as a legal money lender, it must first obtain a licence from the Registry of Moneylenders.

The application process involves reviewing business proposals, conducting background checks on applicants, and assessing whether they are suitable to operate responsibly under the Moneylenders Act 2008. Only applicants who satisfy the regulatory requirements are granted a licence.

This stringent licensing process helps ensure that borrowers deal only with businesses that meet Singapore’s legal and ethical standards.

In case you’re curious, as of the time of writing, the Registry has already stopped issuing new licences.

#2 Grants Licence Renewals

A money lender’s licence is not permanent.

Licensed money lenders must renew their licences annually and continue demonstrating compliance with all applicable regulations. The Registry reviews whether a lender continues to meet operational, financial, and regulatory requirements before approving a renewal.

This ongoing oversight encourages responsible lending practices throughout the industry at all times.

#3 Approves Business Premises

Every physical office operated by a licensed money lender must be approved by the Registry.

Borrowers should only visit approved business premises when signing loan agreements or completing identity verification. This helps ensure that transactions take place in authorised, legitimate locations and reduces the risk of dealing with unauthorised operators.

#4 Conducts Regulatory Oversight & Enforcement

The Registry actively monitors licensed money lenders to ensure they continue to comply with the law.

Its enforcement responsibilities include conducting inspections, investigating complaints, reviewing business practices, and taking disciplinary action against errant lenders. Depending on the severity of the breach, the Registry may suspend, revoke, or refuse to renew a licence.

Why does this matter? Well, these enforcement powers help maintain public confidence in Singapore’s regulated lending industry by holding lenders to high standards.

#5 Publishes the Official List of Licensed Money Lenders

One of the Registry’s most valuable resources available publicly is its official list of licensed money lenders.

Before borrowing, consumers should use this list to verify that a lender is legally authorised to operate—this rings true no matter how enticing a loan offer may be!

Whether you’re considering a local licensed money lender or researching an online money lender in Singapore, checking the Registry’s records can help you avoid unlicensed operators and loan scams right off the bat. It’s seriously the most essential step borrowers should take.

How Does the Registry of Moneylenders Protect Borrowers?

The Registry’s regulations protect borrowers by promoting fair lending practices while reducing the risk of financial abuse.

✔ Fair Lending Rules

Licensed money lenders must comply with the requirements of the Moneylenders Act, which sets clear rules on lending practices.

These regulations include limits on interest rates and fees, as well as requirements for transparent loan contracts that clearly state the repayment schedule, charges, and key terms before borrowers sign any agreement.

This transparency enables borrowers to make informed financial decisions.

Here’s a quick look at the interest rate and fee caps:

- Interest and late interest rate: Max. 4% per month for all loan types, except business loans

- Late payment penalty fee: Max. S$60 for each month of late repayment

- Admin/ processing fee: Max. 10% of the approved loan principal

- Total interest, late interest, admin fee and late fees: Capped at approved loan principal sum

✔ Consumer Protection

The Registry requires every legal money lender to follow strict operating standards.

These include conducting proper identity verification, clearly explaining loan terms, providing written loan agreements, and maintaining complete documentation throughout the borrowing process.

Such safeguards help ensure borrowers understand their obligations before accepting a loan.

✔ Protection Against Illegal Lending

Illegal or unlicensed lenders often use aggressive marketing tactics, misleading advertisements, or unsolicited loan offers to target unsuspecting consumers.

The Registry makes it easier to identify legitimate lenders by maintaining an up-to-date public register of licensed moneylending businesses.

Why should you bother? Verifying a lender before borrowing significantly reduces the risk of falling victim to loan scams or unlicensed moneylending activities—a small price to pay.

Get a quote from a RoM-compliant licensed lender today!

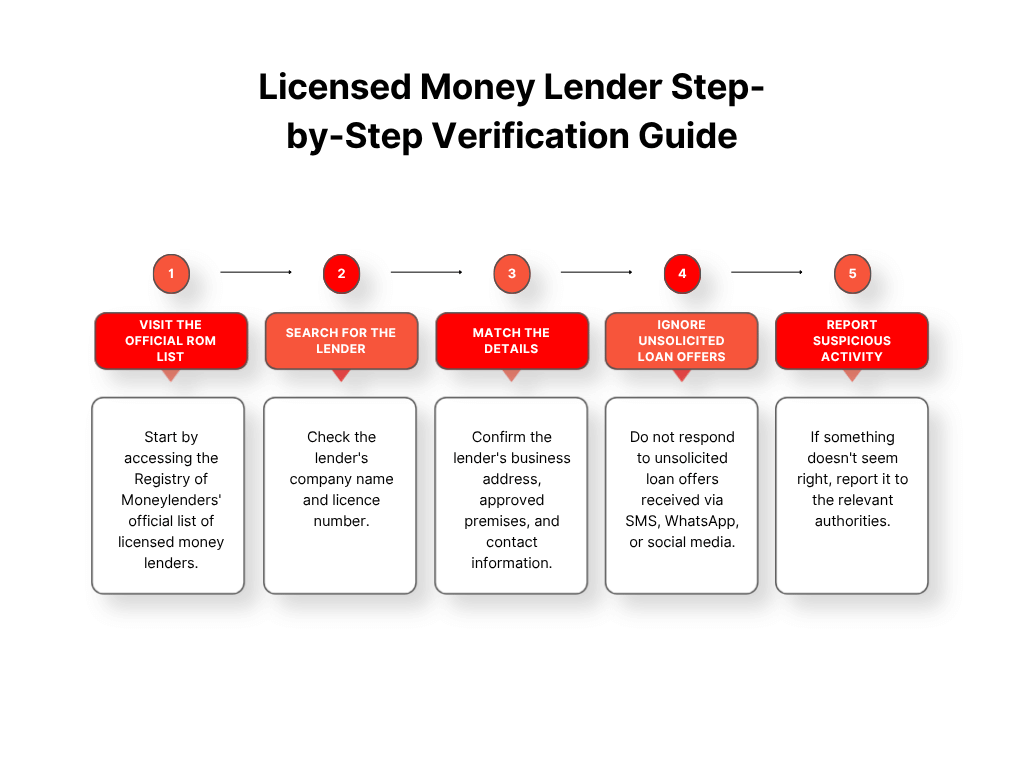

How to Verify a Licensed Money Lender Using RoM?

Follow these simple steps before applying for a loan:

What Does the Registry of Moneylenders Not Do?

Although the Registry plays a vital regulatory role, certain responsibilities fall outside its scope.

The Registry of Moneylenders does not:

- Approve individual loan applications.

- Recommend one licensed money lender over another.

- Negotiate loan terms on behalf of borrowers.

- Cancel outstanding debts or repayment obligations.

- Provide loans directly to consumers.

Loan approval decisions remain the responsibility of each licensed money lender, which assesses an applicant’s financial situation and loan suitability based on its own lending criteria.

Frequently Asked Questions

Is the Registry of Moneylenders Part of the Ministry of Law?

Yes. The Registry of Moneylenders operates under Singapore’s Ministry of Law and regulates all licensed money lenders in accordance with the Moneylenders Act.

Can the Registry Approve My Loan Application?

No. Loan applications are evaluated solely by the licensed money lender you apply to. The Registry does not participate in individual lending decisions.

Does the Registry Lend Money?

No. The Registry is an authorised regulatory body for licensed money lenders , not a lending institution. It oversees the industry but does not provide loans to borrowers.

Can RoM Cancel My Debt?

No. Existing loan agreements remain legally enforceable unless otherwise determined through the appropriate legal process. The Registry cannot cancel outstanding debts. This holds true no matter how indebted you are.

How Do I Know If a Moneylender Is Licensed?

The safest way is to verify the lender’s status on the official Registry of Moneylenders list before applying for any loan.

Can Licensed Money Lenders Contact Me Through Whatsapp or SMS?

Borrowers should be cautious of unsolicited loan advertisements received through WhatsApp, SMS, or social media. If you receive such messages, verify the lender through the Registry before engaging with them. Additionally, always remain alert to the latest police advisories on loan scams.

Conclusion

The Registry of Moneylenders plays a central role in maintaining a fair, transparent, and well-regulated lending environment in Singapore. By licensing money lenders, enforcing the Moneylenders Act, and maintaining the official register of authorised lenders, it provides borrowers with a reliable way to verify whether a lender is operating legally.

Before accepting any loan offer—whether from a traditional licensed money lender, or an online money lender in Singapore—take a few moments to verify the lender through the Registry. As silly as this may sound, doing so can help you avoid illegal lenders and make more informed borrowing decisions altogether.

Need a Loan? Here’s How Soon Seng Credit Can Help

When you need flexible, accessible financing solutions, choosing a trusted legal money lender is just as important as choosing the right loan.

Soon Seng Credit, a licensed money lender in Chinatown, operates in full compliance with the regulations set by the Registry of Moneylenders. Our experienced team is committed to offering competitive loan terms, clearly explaining every loan, carrying out mandatory face-to-face verification, and helping you make informed borrowing decisions with utmost confidence.

If you’re ready to explore your financing options, contact Soon Seng Credit or apply for a loan today. We’ll get back to you in no time! You can safely count on us to provide transparent, responsible, and customer-focused lending every step of the way.